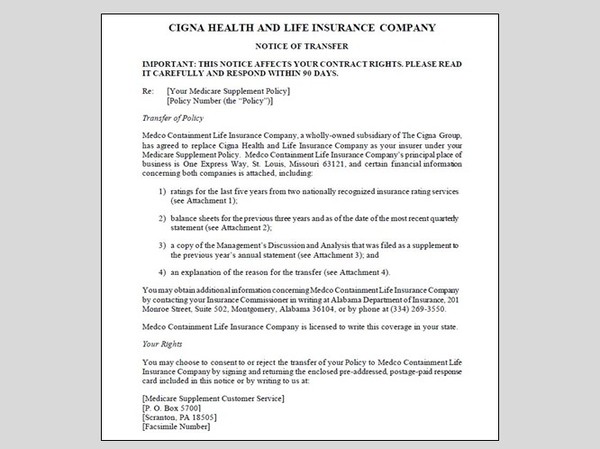

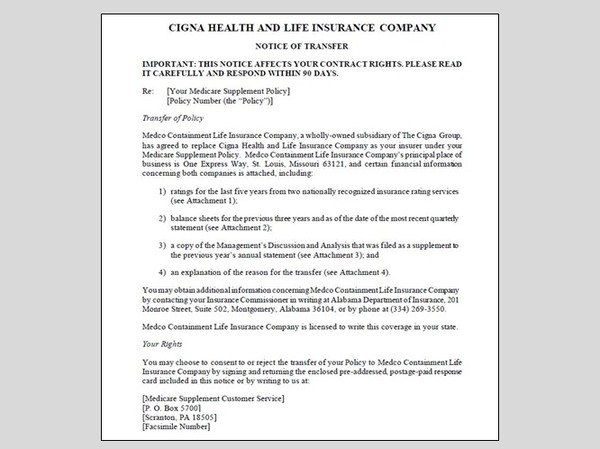

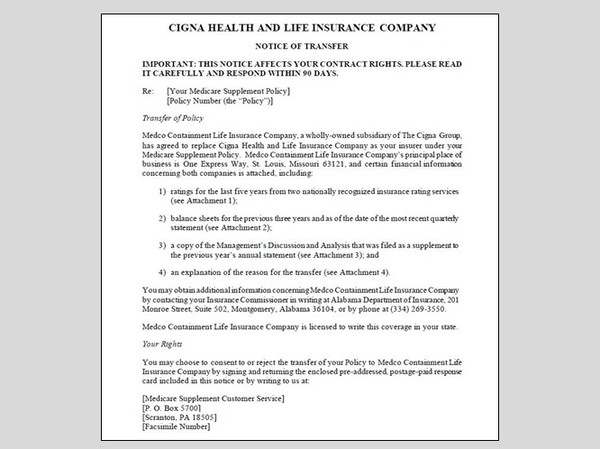

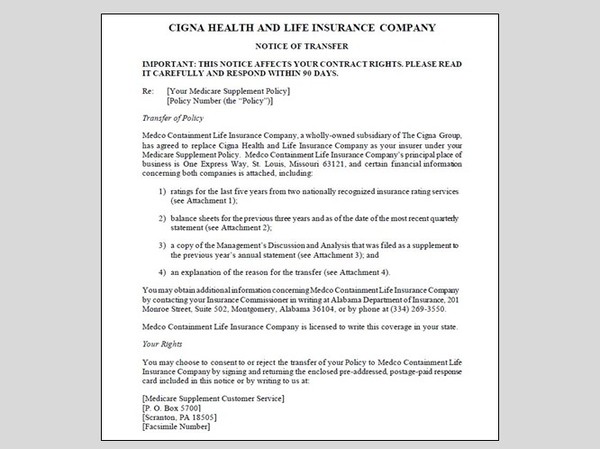

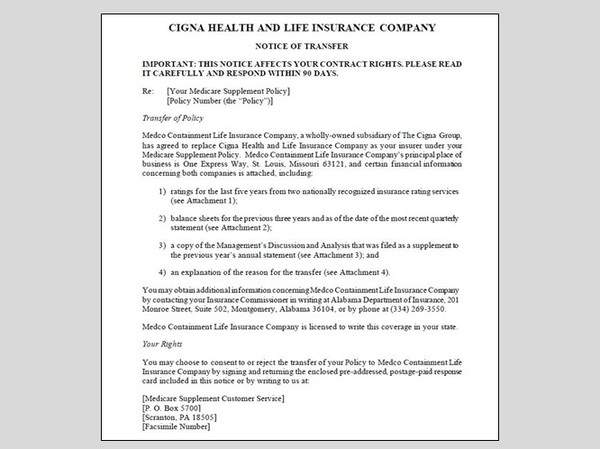

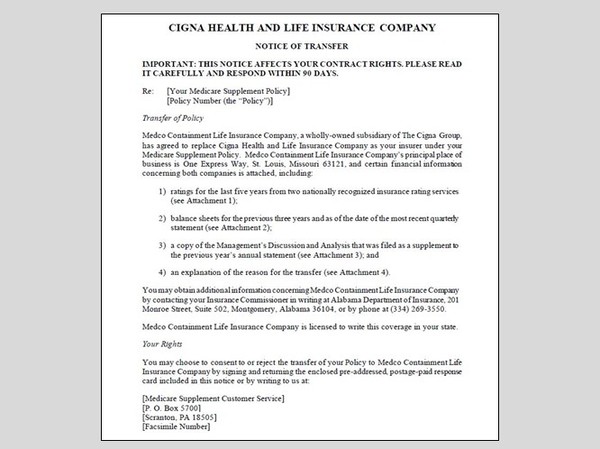

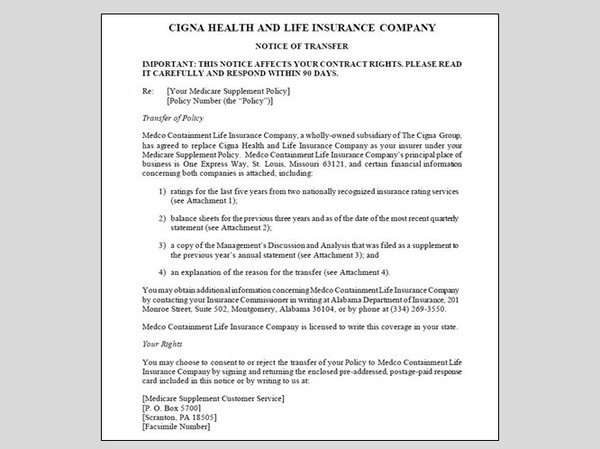

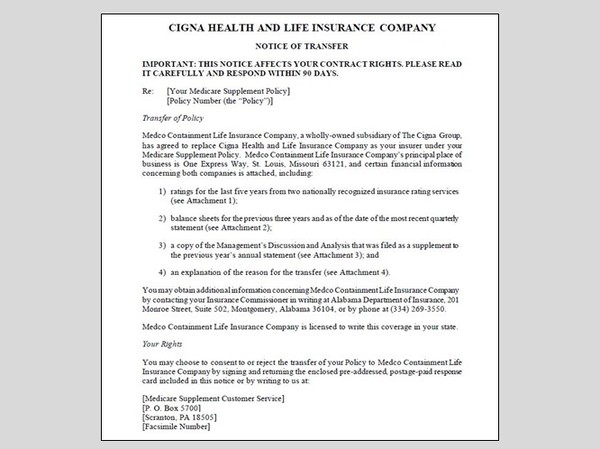

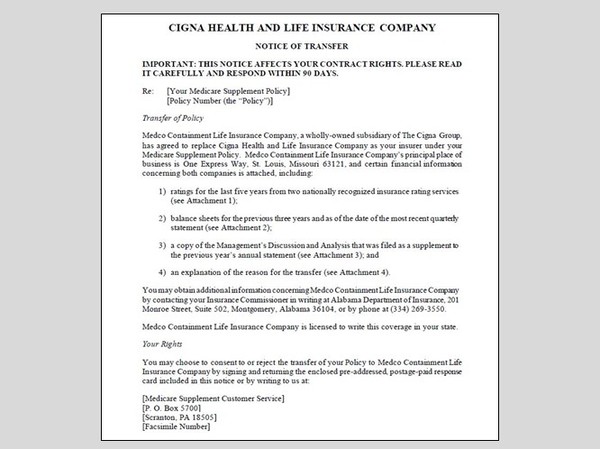

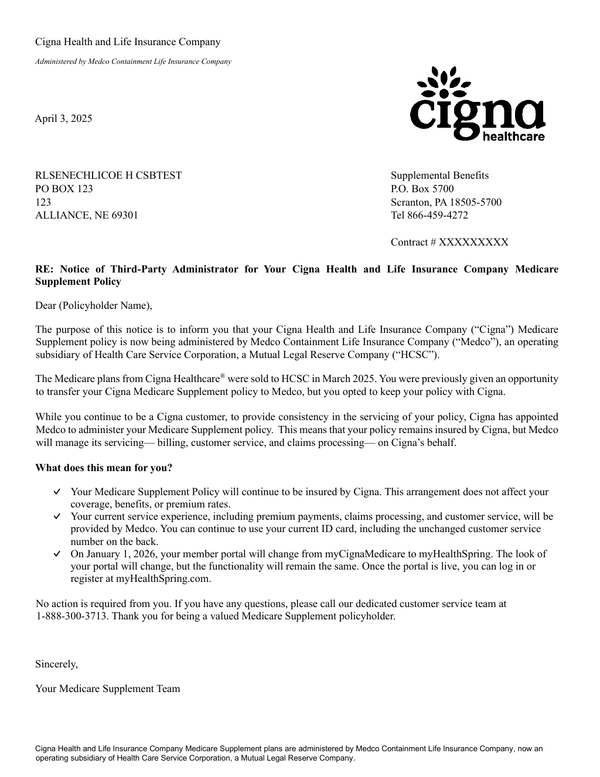

Broker Information Resource

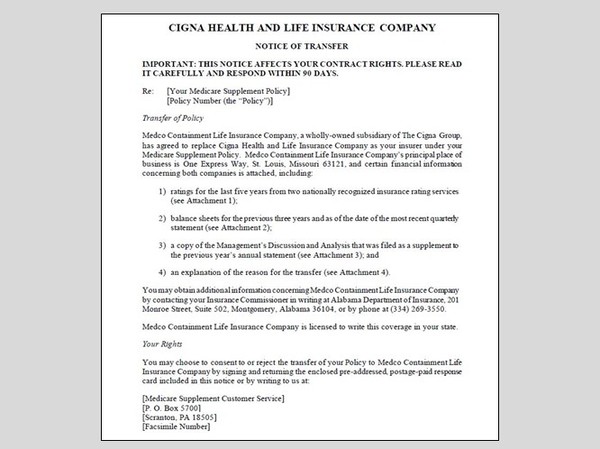

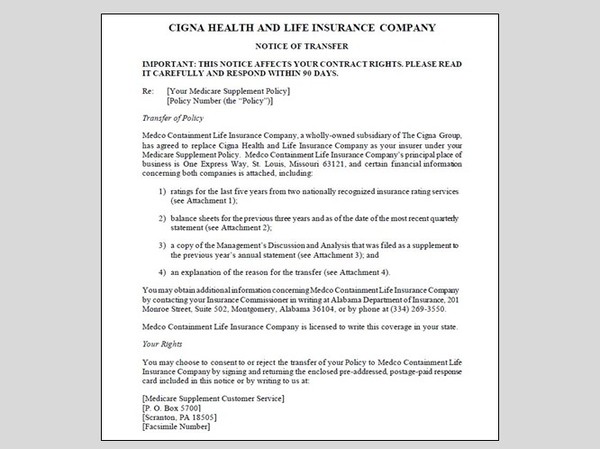

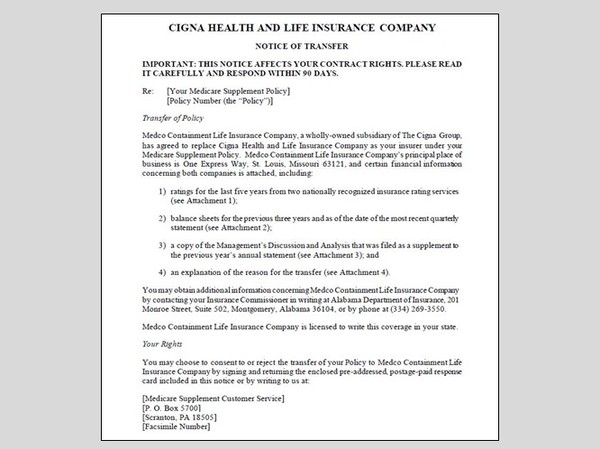

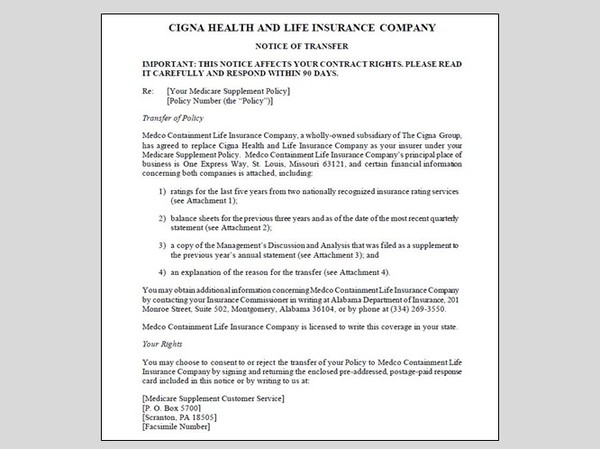

Welcome to the CHLIC transition broker information resource. This page includes CHLIC Transition Frequently Asked Questions (FAQs), Consent Periods by State, On-Demand Trainings, Notice of Transfer - States in Transition (for state Notice of Transfer packets that have been/are being mailed), Notice of Transfer Packet Enclosures (included in all state packets), and Third Party Administrator Notices.

Questions? We hope this resource provides you with everything you need to stay updated on how the CHLIC transition impacts you and your customers. For questions not covered here:

you may call the Agent Resource Center at 877-454-0923 - Monday through Friday, 8:00 AM to 5:30 PM CT.

your customers may call a line set up for CHLIC policyholders at 888-300-3713.

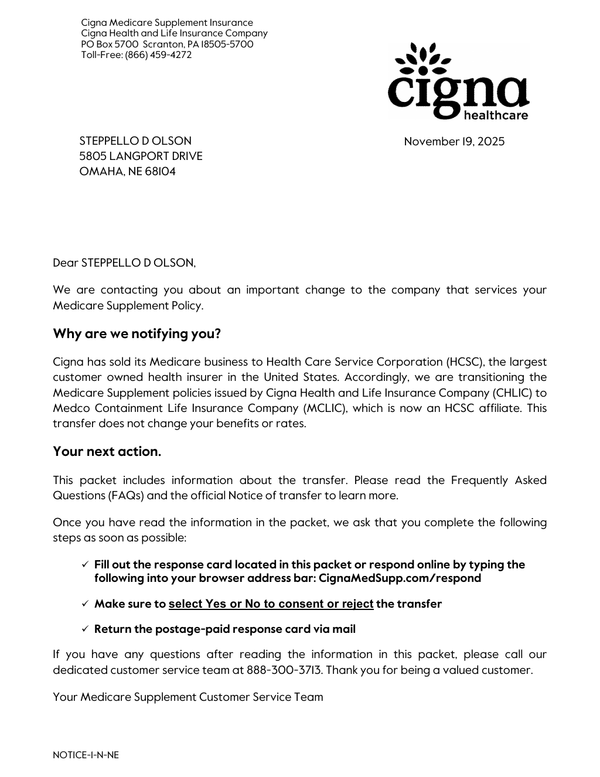

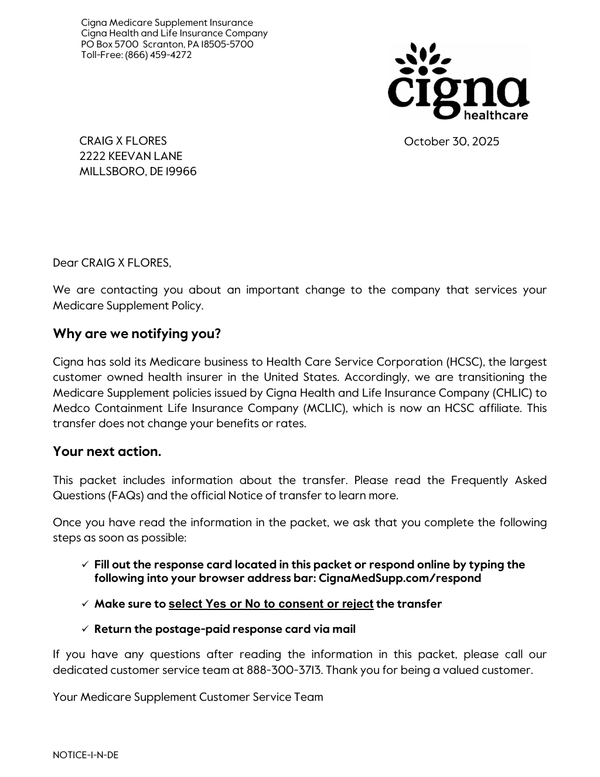

Consent and transition to MCLIC processing timelines: Currently taking longer than anticipated, please bookmark this site and return periodically for updates.